We are willing to look foolish as long as we don’t feel we have acted foolishly.

Warren Buffett’s. Letter to shareholders, 1989

Berkshire started a business called Berkshire Hathaway Reinsurance. It provides insurance to other Insurance Companies. If an insurer wants to layoff his risk, he would pay a premium to BHR and purchase a reinsurance policy. So if an earthquake occurs and leads to a lot of claims for the Insurer, the Insurer would in turn claim from BHR. That way, the Insurer does not go under because of the large volume of claims.

From BHR’s perspective, there could be years when there are no claims and their profits would look excellent. And there could be years when a lot of catastrophes happen like an earthquake in one part of the country, a hurricane in another etc. and they would report huge losses.

BHR plays it smart. They don’t play the price game; they play the probability game. They price themselves high enough such that the expected outcome is always positive. But like I said, in years when there are no catastrophes, the profits will look awesome. But in other years, they could report huge losses. On the whole, over a period of say 5 or 10 years they may earn a very, very attractive return on capital. Charlie Munger once said: we prefer a lumpy 15% to a steady 12%. It should give you an idea of how Buffett and Munger thought.

This business requires two things: a large balance sheet which allows them to absorb the shocks. And the willingness to look foolish in years there are catastrophes.

Investing is akin to BHR. In some years, every move, intelligent or otherwise, will make you look like a genius. In other years, even super intelligent moves will lead to losses.

Therefore, I ask myself:

How foolish am I willing to look?

Stanley Druckenmiller was a protege of George Soros. Together, they shorted the British Pound and they famously made $1 Billion in a single day! He had a track record of having over 30% returns over 30 years!

In 1999, he looked at the valuations of the Internet companies and thought that this is way overvalued. And hence he shorted the market in early 1999. By mid 1999, he had lost money in the short because the overvalued companies became even more overvalued! Then in mid-1999, he changed his strategy and hired two interns and they made long only bets. By end of 1999, he was up 35% for the year.

In January 2000, he sold all his shares. But those two interns didn’t. By March 2000, the interns were up 50% since January. Druckenmiller just couldn’t take it. Here he was – a brilliant man with a brilliant track record watching two interns outperform him! How could they? How could he let them?

And so he invested $6B in March 2000. He ended the year 2000 with a loss of $3B.

When he sold all his shares in Jan 2000, did he act foolishly? No he didn’t. In fact, even when he had shorted it in 1999, he had acted with intelligence. But that is the nature of the market. Even when you act intelligently, you could end up with terrible results. And those interns who weren’t smart enough to sell in January 2000, ended up looking brilliant by March.

But was Druckenmiller willing to look foolish? Alas, no! That was his Achilees heel.

Compare that with Warren Buffett.

Buffett said he did not understand Internet companies and chose to not invest in any of them.

Did he look foolish? Oh yes! Everyone and their brother was making more returns than Berkshire did.

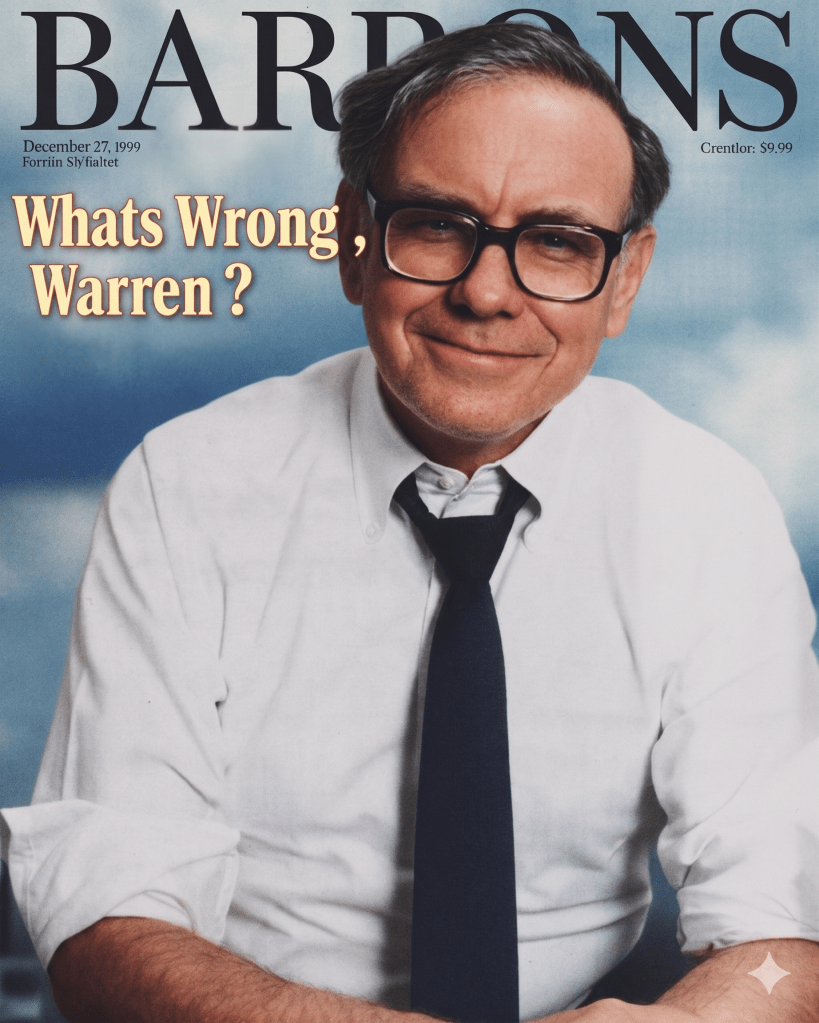

Was he okay looking foolish? Yes. In fact he didn’t care what the world thinks about him. Even if he was questioned on the cover page of a magazine in December 1999.

Both Buffett and Druckenmiller were brilliant at their game. But the principle difference was, in my opinion, that Buffett was willing look foolish; Druckenmiller wasn’t. An unwillingness to look foolish even when you have done your homework can lead to mistakes.

—

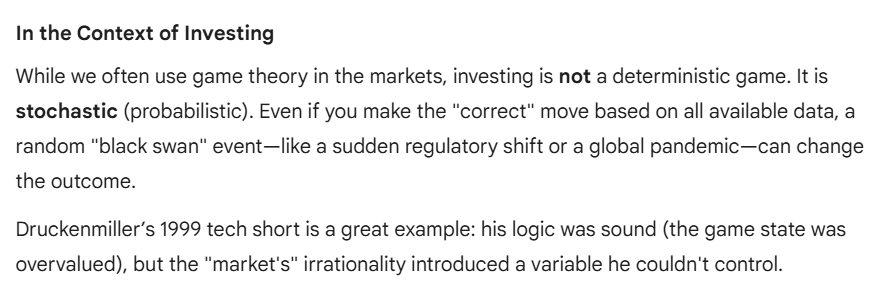

A deterministic game is one where you progress from one level to another without an element of luck. There are no dice rolls and there are no probabilistic events that can shape the outcome. Like say Tic-Tac-Toe.

On the other hand, in a probabilistic game the outcomes are not entirely in your control. You could play brilliantly and yet lose. Or play casually and win. Most games fall in this category – like modern day Cricket or Football. Even Investing.

We all want to win. Even if you work hard and play well, the result isn’t entirely in your hands. When I see reporters writing about how hard the winning team trained and how well they prepared, I think to myself: even the team that lost, probably trained hard but they may have been just unlucky to not win.

Likewise, in investing, the outcome is not entirely in your hands. For example, I own some good companies that I bought after studying them and I bought them when they were cheap. Now they are cheaper. I did not sell IEX at a valuation of 100 X PE and watched it become 25 X PE. I sold BSE at a valuation of 75 X PE and watched it go up another 600%. Buffett and Munger loved Walmart as a business but refused to invest in it because it was expensive and they regretted it too. These kind of anomalous outcomes are not a bug; they are a feature of investing and business.

If you invest for long enough, you are going to find these patterns play out again and again. If you say to yourself, I will be a disciplined seller- you will not make IEX kind of mistakes. But you will also miss out on some large multi baggers (which may make a difference to your final outcome). If you say, you will buy and hold for a long time, you will have many multi baggers but you may end up with something like IEX. My point is this: when we decide to buy, sell or hold, we do so with limited information and hence, even our good decisions have a good chance of going bad.

All bad outcomes are not because of you. All good outcomes are also, not because of you. Don’t beat yourself up when your favorite ideas don’t do well. Don’t pump yourself up when your favorite ideas do well. Luck has a huge role to play in the final outcome. What we see is just one outcome among a wide range of outcomes. Therefore, have gratitude and be contented. This is what will help you mentally survive a long game.

And yes: be willing to look foolish even when you haven’t acted foolishly. That would make you a Teflon coated investor.

-Cheers!

Good one Vikas. Just one comment – Holding long enough has to be backed by growth assumptions reamining intact. When that assumption is challenged the long term investor should act before its too late. Thats the takeaway for me for IEX. For BSE the usual problem of overestimating short term results and underestimating long terms results were in play. Ofcourse, investing is a life long journey , there will be breakdowns and there will be many hits providing a good learning platform. Humility is the way to become an intelligent investor.

LikeLike