“The Great, The Good and The Gruesome” is my favorite essay of Warren Buffett. This was written in February 2007. In it Buffett writes about the great businesses like See’s Candy which has a very high Return on Capital and requires almost no capital to grow. He also talks about a good business like Flight Safety, which has a moderate Return on Capital and requires more capital to grow. And finally, Buffett’s punching bag (gruesome business) is the Airline industry which neither has a good Return on Capital nor can it grow without capital.

—

But what works for Buffett does not work for you and me. See’s Candy for example, has had almost no growth. So they send all the profits to Buffett and he uses it to acquire other companies. So while it’s okay for See’s Candy dto not grow, Berkshire does by using the capital sent by See’s.

Last year See’s sales were $383 million, and pre-tax profits were $82 million. The capital now required to run the business is $40 million. This means we have had to reinvest only $32 million since 1972 to handle the modest physical growth – and somewhat immodest financial growth – of the business. In the meantime pre-tax earnings have totaled $1.35 billion. All of that, except for the $32 million, has been sent to Berkshire (or, in the early years, to Blue Chip). After paying corporate taxes on the profits, we have used the rest to buy other attractive businesses. Just as Adam and Eve kick-started an activity that led to six billion humans, See’s has given birth to multiple new streams of cash for us. (The biblical command to “be fruitful and multiply” is one we take seriously at Berkshire.)

Warren Buffett, Letter to Shareholders 2006

But Why do I say it won’t work for us. A company that earns a very high Return on Capital but does not grow will return capital back to us in the form of dividends and/or buybacks. Firstly, these are tax inefficient ways of returning money. Secondly, the onus will now be on me to find other opportunities to invest and earn good returns. Thirdly, in a country like India where the economy itself is growing, the market does not reward companies that aren’t growing.

So we need to tweak what Buffett is saying slightly.

So, we want business whose core business is so profitable that it throws a lot of cash and the management is willing to invest that money in growth, like expanding capacity, adding more products, investing in R&D, sales, technology etc. That way, they create optionalities for me as a shareholder. The optionality is: if the new venture fails, the company loses some money, but if the venture succeeds, then we reap the benefits. This is one of the big secrets: we need optionalities.

Let me share a couple of examples from what I have observed- Bajaj Finance and Eicher Motors.

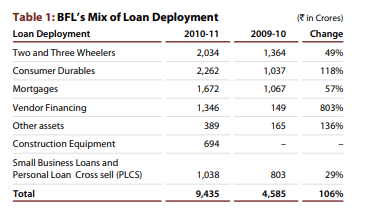

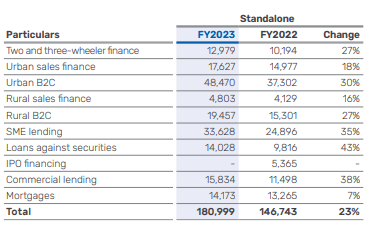

Bajaj Finance started with just one product: Two and Three wheeler loans. By 2011, they had about products.

Now not all of them clicked. For example, they lost money in Construction Equipment and exited that business. Today, they are present in about 11 product lines.

Their loan book has grown by 100 times between 2008 and 2023! How did they do that? They did that by adding more product lines, going to deeper parts of the country, investing in people and technology etc. It is a rather simple playbook but the key has been great execution.

—

Eicher Motors manufactures the Royal Enfield brand of motorcycles. In 2010, they manufactured 52,576 motorbikes. In FY 2024, they manufactured 912,732 motorbikes. That is a modest 18X growth as compared to Bajaj Finance. How did they do it? They did it by heavily investing in R&D, by setting up dealerships in different parts of India as well as going international, by bringing out beautiful products etc. In fact they have taken the fight to the Japanese by setting a dealership in Tokyo. Again, in my opinion, the playbook is simple while the key has been the execution.

—

I usually get excited when I find a company that has a very profitable core business and it uses the profits to grow. Ideally I want the company to invest in the new venture using the profits and not through equity or debt. (Sometimes though my businesses do infuse equity or debt for growth but I tend to forgive them.) Even if the new venture fails, like Bajaj Finance and the Construction Equipment business, it’s okay because the core business is quite strong. But when the new venture succeeds, there is no limit to how much we gain.

Optionality is: heads I win a lot, tails I don’t lose much. (Fragility is: heads I win, tails I die).

—

Therefore, we need to take what Buffett says (high quality business, high Return on Capital) and add a little tweak. Berkshire Hathaway is a conglomerate and can take profits from one subsidiary and invest in another or acquire another subsidiary for the growth of conglomerate. Therefore we need companies that can take profits from one line of business and invest in another for growth.

-Cheers!