Below are a pair of statements. Identify the more possible ones.

- 1A: A massive flood somewhere in North America in which more than a thousand people die.

- 1B: An earthquake in California, causing massive flooding, in which more than a thousand people die.

- 2A: Joey seemed happily married. He killed his wife.

- 2B: Joey seemed happily married. He killed his wife to get her inheritance.

- 3A: Linda is a bank teller.

- 3B: Linda is a bank teller and is active in the feminist movement.

(These examples are taken from Thinking Fast and Slow and The Black Swan.)

If you selected any B, then: Congratulations, you are human but also incorrect! The As are the correct answers.

In the first example, California is a place in North America. Floods that happen in California will be counted in California and North America, but floods that happen elsewhere in North America will not be counted in California. Therefore, Californian floods by definition are a subset of North American floods. And hence the chances of North American floods are always more than Californian floods. Same logic with the other examples.

But, but, but …. option Bs are more descriptive. There is so much news of Californian wild fires, so we assume it is also a place where floods can take place. And hence it seems more possible. And we fall for it.

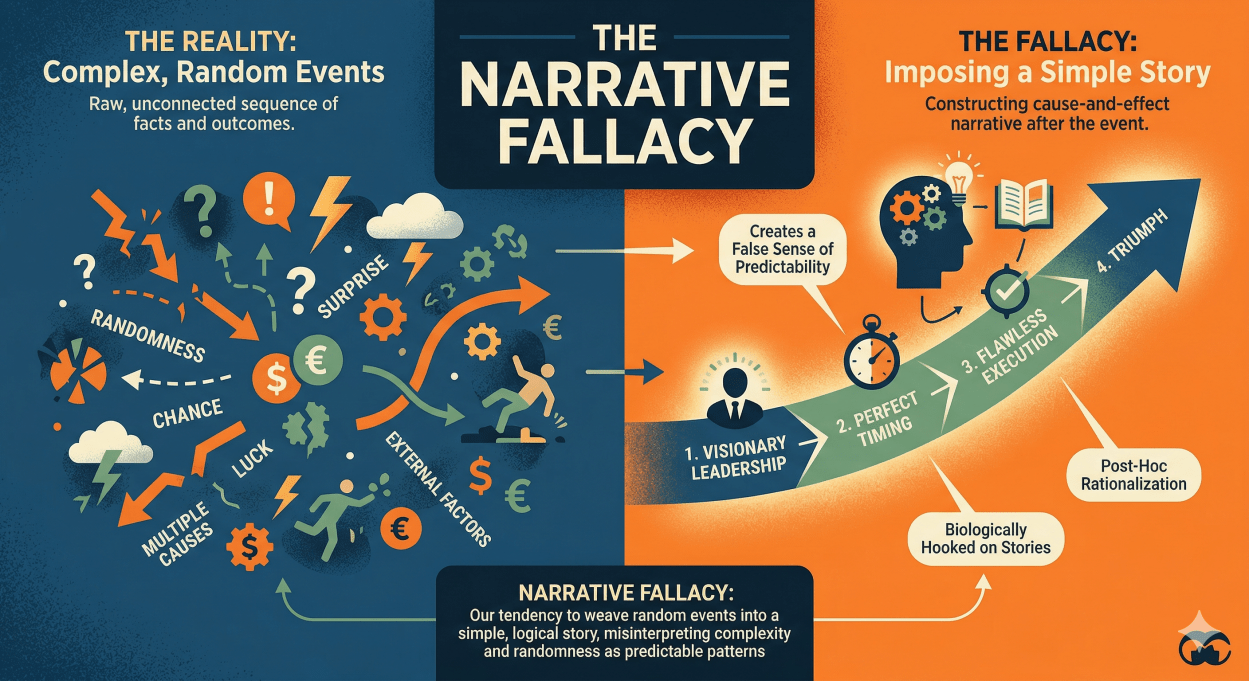

That is Narrative Fallacy.

You see, our minds are not wired for complexity. Our minds compress complexity into simple narrations. Storing random events in the brain is harder. But by weaving a narrative around those events, it makes it easy to store, retrieve and retell stories. As time passes by, we forget that these are just stories and we simply take them for facts.

—

What kind of an investor are you?

Blue chip only? Quality? Micro cap? Growth at reasonable price? Buy at any price? Momentum? Value? Passive? Some other type?

Now consider the following set of examples and list the one that is more possible.

- 4A: Warren has successfully invested in many multi baggers.

- 4B: Warren has successfully invested in many multi baggers because he is a micro-cap investor. Many of his investments were small companies that have grown multi-fold now.

Since I have primed you to spot the narrative fallacy, you will tell me that B is a subset of A and therefore the chances of A is higher than B. Everything that the second Warren has will count for the first Warren too, but there could be investments in large companies that became multi baggers that the first Warren has which wont count for the second Warren. And hence there are more chances of finding the first Warren than the second.

You will also tell me that even though B is more descriptive and “seems” more possible, it is A that is more probable in reality.

Very good.

There is another assumption that is not true. That is: large companies are slow growers while small companies are fast growers.

The truth is that some small companies can grow fast. Another truth is that some large companies can also grow fast. But like I said, over time we mix up narratives for facts. Some small companies grow fast morphs into all fast companies are small companies.

To think that all small companies can grow fast is incorrect. It is like looking at the world with only a Physics lens. We need to temper this with some Biology. An elephant is 10,000 times the size of a rat. Yet, its metabolic rate is just 1,000 times. In other words, the elephant’s internal cells and organs operate at a much higher efficiency than that of a rat. A rat lives for about 3 to 4 years; an elephant for 75 years.

You can compare all the operating metrics of say a Bajaj Finance and a similar smaller company and you will see that the larger animal is not always inefficient. A large company has a larger budget for R&D, marketing, training, software development etc. The kind of experiments that Bajaj Finance is doing with AI and Account Aggregator is mind boggling. As a % of the AUM, these costs may be less than that of the smaller company. Like elephants, some big companies can be more efficient.

There are some large companies like ICICI Bank (40% CAGR), Bajaj Finance (26% CAGR), Mahindra & Mahindra (113% CAGR), Canara Bank (61% CAGR) that have grown their profits fantastically over the last 5 years.

Likewise, I don’t buy the argument that just because a thousand analysts are following a company, it is efficiently or correctly priced. If that were the case, then all those analysts must have made a fortune investing in Mahindra & Mahindra. But it is not the case. Even well-paid analysts can miss the forest for the quarterly margins.

So, it’s not a foregone conclusion in my mind that only small companies can grow fast. In my mind, some large companies can grow fast as can some micro companies. Therefore, why should I restrict myself to a smaller pool of only micro caps? If a micro company fits my criteria, I will invest there. If a large company, fits my criteria, I will invest there too.

To give a cricket analogy. Why would I want to score runs only on the leg side when I have the entire field?

Investing and the Business of Investing

When we think of Dove soap, we think of a soap that has moisturizer and is gentle on the skin. When we think of Lifebuoy (also made by HUL), we think of a soap that is tough on germs. Gentle and tough are narratives created by HUL and placed in our minds. It then becomes easier for HUL to sell its soaps.

Investing and the Business of Investing are two different things. Investing is what I do – I try to find investible ideas across the entire spectrum of companies. Business of Investing is what HDFC AMC does. It launches many schemes depending on the mood of the market. More the AUM it garners, more is its revenues and profits. It is a business like HUL. And therefore, it sells different products through different narratives (Blue chip, Manufacturing focused, Defense focused, Value focused, Technology focused etc.).

For HUL and HDFC AMC, it makes sense to create narratives which makes it easier to sell products.

But you and I are investors. And we must be opportunistic. If opportunities invest in large companies, then we must pay attention to them. If opportunities arise in micro companies, then we must pay attention there too. Labels are good for selling; lack of labels is good for investing.

—

So – let me ask again: What kind of an investor are you?

Correct answer: The one that makes money.

More power to you!